The EVolution #25: Unplugged

The EVolution #25: Unplugged

A sad coda for excessive ambition and SPAC mania

For companies with avian branding, it’s been a “fowl” month. Leave aside the debacle at Twitter caused by Elon Musk, out-of-scope for this newsletter. Bird, the electric scooter rideshare service which went public via SPAC in Nov 2021, revealed it overstated its revenue for the past two years. Bird also warned it doesn't have enough cash to cover operations for the year ahead.

Then there’s Volta. I’m gutted to see my former employer, a decade-old business and operator of 3,000+ EV charging stations, in dire straits. From their Nov 14 10-Q report:

Management believes that the Company’s cash and cash equivalents [$15.6M as of Sep 30]…are not sufficient to meet our working capital and capital expenditure requirements for a period of at least 12 months from the date of issuance of this report… No assurances can be provided that additional funding will be available at terms acceptable to the Company, if at all.

This year already saw an almost total replacement of Volta’s executive team, multiple rounds of layoffs, and an untenable burn rate for an unprofitable company. The collapse has been dramatic. It was only Aug 2021 when Volta went public at around $10/share, raising ~$400M through SPAC + PIPE fundraising!

Given my emotional attachment to Volta’s mission and to so many of its past and present employees, I think it's important to clarify lessons learned that should be applied to charging network operators, and more generally, to any growth-stage startup.

Hero to near-zero

Not long after we began publicly trading, I had a chance out-of-town run-in with one of our executives. A lengthy chat led to this frank exchange:

ME: Alright, best guess—what will our stock price be in six months?

EXEC: $20, maybe a bit higher. What do you think?

ME: I hope you’re right. But, umm… $6-$7? The targets in our SPAC deck were very aggressive, and after two quarterly earnings reports I think the Street’s gonna punish us if we miss.

Well, we were both wrong, and I took no joy in being directionally correct. The week of our second earnings report, VLTA closed at $2.19. The broader stock market correction had arrived, and so had the reckoning for nutso SPAC projections I called out long ago (where I said “earnings calls are wakeup calls”). But that wasn’t all.

Volta, having admitted to “material weaknesses [in] internal control over financial reporting,” exacerbated its position by amending its first quarterly earnings report and indefinitely canceling the release of the second. Shortly after, the company’s co-founders—the CEO and president—resigned. Another executive, a newcomer to EV charging, briefly served as “interim CEO” before being replaced by Volta’s chairman, who was our SPAC sponsor. The latter is still in that “interim” role and the CFO position has been empty for months.

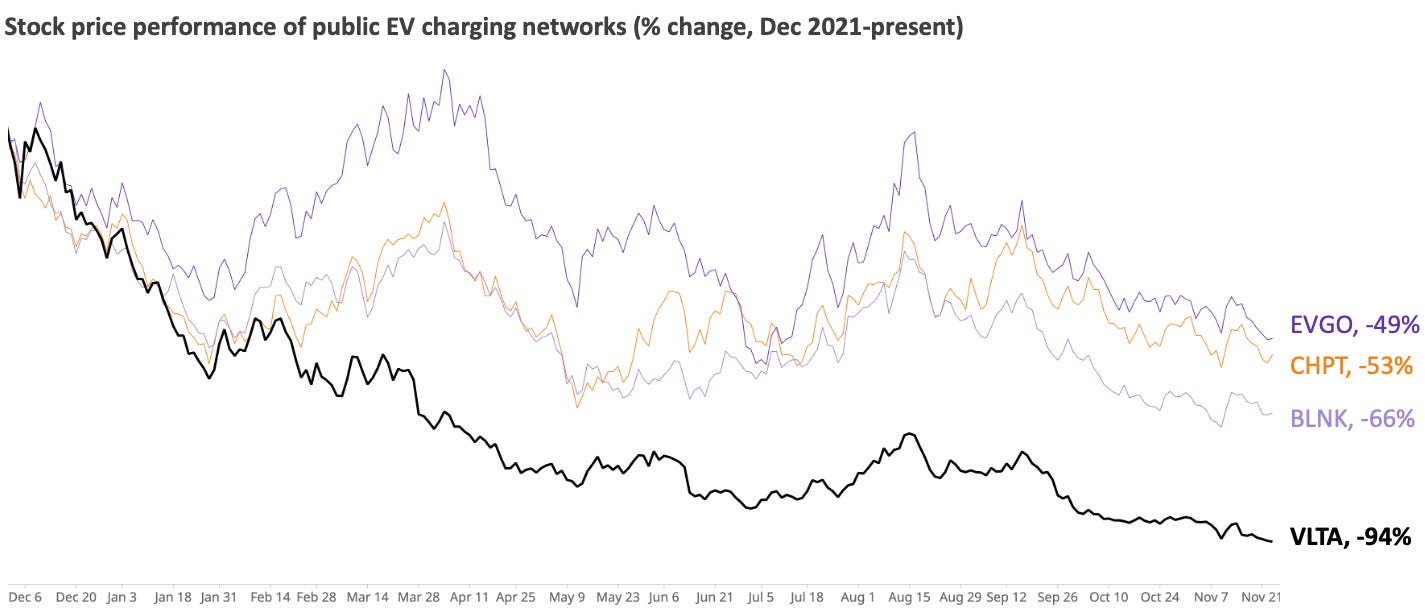

By October 2022, VLTA dipped below the $1 mark and was worth a fraction of competitors whom we once rivaled or dwarfed, like EVgo and Blink. The company instituted abrupt mass “furloughs,” executed shamefully. A majority of employees had their salaries, healthcare, and benefits suspended; equity grants to long-time staff were canceled just days before their vesting date; no severance pay was given; and not a word was communicated from leadership to those affected. It was an unconscionably poor way to treat committed workers.

Volta was never a “meme stock” nor a stay-at-home pandemic fad, two kinds of companies now associated with massive reversals of fortune. Even so, while valued at over $2 billion last fall, Volta’s market capitalization today is just $99 million.

“I got a bad feeling about this…”

Funding is the lifeblood of most high-growth startups. But even with money in hand, things can go off the rails pretty quickly when those rails haven’t been laid in the right direction. Volta’s problems pre-dated life under Wall Street’s scrutiny. Back in April 2020, as part of formal feedback to our leadership team, I wrote both about positives and areas where we needed to improve. Among the latter:

Lack of [senior-level] accountability is a serious issue. From the top down we don't make very good use of meetings; people don't engage with content, don't come prepared with questions, don't offer *constructive* criticism and feedback…

The targets the company sets and the narrative being pitched externally are not buttressed internally by a solid road map of how to achieve those things... No concrete plans, timelines, requirements, and accountability.

Company goals are a joke. We never come close to hitting them, but worse than that (given many startups have lofty goals) we don't structure our operations to even try to hit them, or know if we could ever hit them, or why we're falling short.

In summer 2021 I wrote a “SWOT” analysis for a few of our leaders. While also highlighting many things we did well, I called out items that worried me, including:

[Volta’s] poor understanding of, and/or responsiveness to, cost drivers, revenue trends, forecasted gaps, and measurable market conditions

Profitability/unit economics threatened by shift away from a deliberately smaller footprint of mostly highly-media-attractive sites toward a comprehensive national charging network with majority of revenue to come from [charging drivers to fuel]

Divided executive attention — between SPAC process and European expansion, far less focus from the top on actual business performance

Capital markets scrutiny — SPAC bubble appears to have burst; quarterly earnings reports will be closely scrutinized against aggresive [sic] targets set during fundraising

Ever the optimist, I believed our issues were fixable if leadership would actually acknowledge them. The conviction that Volta’s core business model was solid; the dramatic increase in support for electric vehicles from the public, automakers, and government; and love of our mission of making EV adoption easier for thousands of drivers—these factors kept me genuinely hopeful.

Lessons for EV charging

We didn’t need to chase ludicrous growth targets. In 2020 and early 2021, investors were far less attuned to EVs and charging infrastructure. That was the moment to define realistic expectations of and for the industry, as well as increase our own standing due to the unique nature of our business model.

I’ve blogged before about the economic structure of the fueling business, and how one must either accept low margins or do something additional for revenue (like gas stations with mini-marts). Volta’s original business strategy was small footprint and high margin:

Install relatively inexpensive “L2” charging stations, bundled with advertising billboards, selectively at retail locations popular with shoppers and desirable to advertisers

Attract drivers and generate goodwill by offering charging for free—feasible with L2 energy amounts small compared to fast-charging (“DCFC”) stations

Over several years, in sync with increased EV adoption by the public, add additional stations (whether L2 or for-pay DCFC) at existing locations that had proven demand for advertising or charging

I credit our founders for originally devising and implementing this model. It worked very well when executed correctly and, I’m confident, still has a lot of room to run.

Where Volta went wrong, in my opinion, was chasing valuation and status in a frothy market that had just caught EV fever. Our CEO had long scorned “charging for electrons” in mass, but suddenly we were copying the heavy footprint model and seemingly downplaying the ad business responsible for the majority of our revenue. Leadership now claimed we’d rapidly install thousands of new stations nationwide and quickly generate significant revenue from paid charging.

“Construction projects are often completed ahead of schedule and under budget!” — No one, ever

But building out infrastructure has certain immutable realities, among them that it is costly, that acquiring jurisdictional permits can be very time-consuming, that negotiating contracts with property owners to operate on their sites can be a byzantine process, and that for DCFC stations many sites need extensive utility upgrades that take ages to happen.

Accepting payments is a deceptively complex endeavor, too, which involves solving for a plethora of hardware, software, data, and connectivity challenges. Stepping into this arena also introduced Volta to new regulatory, security, privacy, and customer service issues, and necessitated a major pivot in our branding and go-to-market approach.

The infusion of funding from going public could have been devoted fixedly to these critical areas. Instead, Volta began pursuing even more aggressive expansion and buzzy trends. Launching in Europe; trying to win industrial and commercial fleet charging business; investing in and marketing our AI/ML capabilities; developing bespoke software… It was a lot to bite off!

This led to hiring too many people who, despite their talents and dedication, were mostly aimed at areas where we either didn’t have a ”right to win” or which would not move the needle from an economic standpoint anytime soon. Trying to do too much resulted in Volta spending a ton of money and yet doing most things poorly.

To this day I remain baffled at the relative lack of focus on optimizing our advertising business—which nonetheless continues to show revenue growth and has proven its viability in several major markets across the country.

Lessons for high-growth startups

Even for growth-stage companies completely unrelated to the world of EVs and charging, many key lessons apply:

Be realistic about how much complexity your business can handle at once

Focus on building your core advantage and don’t mimic competitors’ products, features, or sales strategies without carefully considering whether you have the ability, incentives, and right to win there

Ensure that technical constraints and development timelines are well communicated to, and understood by, individuals making business-side decisions

Before taking on money, confirm that investors’ growth expectations are in alignment with yours, and that those present an acceptable risk-reward calculus

For org scaling, distinguish between work that requires permanent, full-time headcount versus what really are short-term projects that can be handled by existing (likely cross-functional) personnel

Manage cash flow even in good times, have contingency plans thought out in advance, and don't dither when it’s obvious an iceberg is ahead

Moreover, leadership really matters. A management team needs to ruthlessly prioritize, not let the company chase “shiny objects,” and exercise restraint after an influx of funding to avoid scope creep and organizational bloat. Humility is a must. Good leaders are effective judges of which voices in the org to elevate, and they actively seek out internal subject matter experts who can test and challenge their thinking.

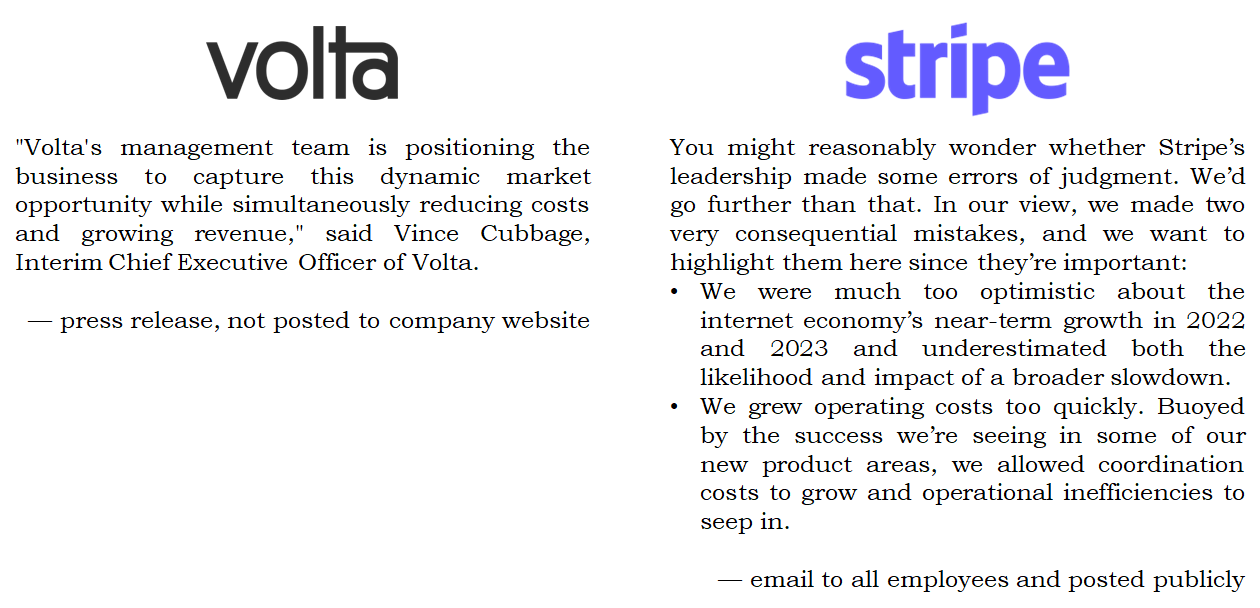

Finally, it's easy for an executive to think of oneself as a leader and celebrate their company culture—until that’s put to the test, having to own up to getting something wrong. Then cue the boilerplate comments about market conditions and macroeconomic headwinds… Compare the anodyne statement by Volta regarding its “furloughs” versus how Stripe’s leaders took responsibility for mass layoffs.

Parting thoughts

I’ve talked extensively with many of my former co-workers, and know a lot of us have similar takes on why things went wrong. Other folks who have been a part of the Volta journey may have their own opinions, and I’m eager to learn from their perspectives, too.

I was deeply committed to Volta, and reckon that I was in the longest-tenured decile of employees at my departure. I’m proud of the work I did, reflected in a record of positive performance reviews and successful projects that had material impact on revenue generation, cost savings, information flow, and company culture.

Most importantly, I’ll cherish a great number of friendships and professional relationships from these past few years. There are many talented colleagues who will be valuable assets—either trying to right the ship at Volta, or at their next employers—hopefully continuing to dedicate their efforts to fighting climate change!

Drive forward.

This should be required reading for all startup, A-series, SPAC-hunting and angel stage businesses. Never mind EV, it applies to every market. When the investors want management to chase shiny objects and muddy the deck, it’s up to leadership to tell them “no,” value comes from keeping it simple, doing it right, challenging assumptions, and planning for success too to bottom. It’s better to pivot and take a hit than to build a meringue pie and collapse.

“Top” to bottom